*Originally published in Benefits and Pensions Monitor

Planning and saving for retirement is too hard for most Canadians.

Seventy percent of Canadians are worried they aren’t saving enough for retirement, and 62% are concerned they will outlive their retirement savings.

Unlike in our working years when the goal is to accumulate funds to maintain a quality standard of living in retirement, the later phases of life when those savings are steadily drawn down can expose overlooked risks and misconceptions about budgeting in retirement.

Part of the challenge is that many Canadians underestimate the true cost of retirement. Housing, health care, transportation and food expenses add up quickly, and tend to rise over time with inflation, especially with increasing longevity.

Another challenge is the behavioural shift from building or “accumulating” savings during one’s working years, to drawing down or “decumulating” savings without a steady income source in retirement.

As difficult as we know it can be to plan and save sufficiently for retirement, Canadians encounter a bigger challenge learning how to spend those savings prudently to last a lifetime.

The risk is real because many don’t have the skills or access to solutions that spread their savings efficiently in retirement, which need to account for:

- Longevity risk – outliving one’s savings, which is a significant concern for most Canadians.

- Tax efficiency – decisions around deferring government benefits or starting early, or whether to draw down from the TFSA or RRSP first.

- Market volatility and inflation – the risk of cost-of-living expenses increasing over time and the ability of their savings to withstand downturns.

- Minimizing fees – assessing the marketplace of drawdown options to ensure the chosen vehicle fees do not erode their savings and ultimately standard of life.

Modern defined benefit (DB) pensions are simple, flexible, cost-effective and last a lifetime. These cost-certain plans are now available to all Canadian workplaces. However, Canadians want additional options to tailor to their needs in retirement. I believe it’s time we look at the lifetime retirement income design options that will better help Canadians meet their goals.

Decumulation designs address an existing and growing gap

According to a report by the National Institute on Ageing, individual retirement savings accumulation accounts now hold more than $1.5 trillion nationwide. Retiring Canadians are “trapped between two extreme and inadequate decumulation options: buy a life annuity from an insurance company or move their accumulated savings into a personal retirement income fund, where they must individually manage the fund’s investment and drawdown.”

There is an enormous pool of savings in need of better

management. Pension innovators can step in to fill the

market gap.

Large pension funds benefit from scale and risk pooling that are out of reach for individuals through access to unique asset categories and much lower fees, both of which financial experts know are key to compound value and growth over time. Then there is the expertise. Many of the large Canadian pension plans are some of the most admired and well-managed in the world – and trusted by members.

The Canadian pension industry has world-class models for a sustainable, valuable, and efficient retirement vehicle, in the form of a DB pension. What if we created comparable vehicles that open access so that more Canadians could benefit?

The business case and economic benefits are clear. The missing piece is an efficient solution that is accessible to all savers and delivers what Canadians need most in retirement: reliable lifetime income to help achieve a quality standard of living.

Canada has many accumulation options. It’s time to broaden retirement plan designs to capture the decumulation life stage and provide cost-effective retirement income for life. These are basic needs that retirement industry leaders have the resources and responsibility to address.

Retirement literacy should cover the whole lifespan of senior living

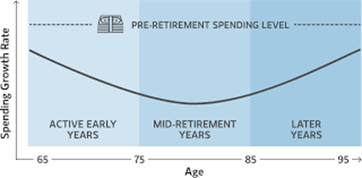

Setting and sticking to a sustainable retirement spending plan is a daunting task. Some will overspend on recreation especially in their early retirement years, while others will conserve out of fear and sacrifice quality of life, leaving behind much of their savings unenjoyed.

Risk tolerance, expenses, and lifestyle standards fluctuate over time. Increased spending often occurs when workers “cross the finish line” and spend to celebrate being work-free, and again in the later years when expenses like health care can increase substantially. This drives dynamic changes in income needs.

Source: Morgan Stanley Wealth Management as of June 2019

Conventional financial literacy treat retirement as a finish line, yet the average Canadian should budget for 30 years in retirement. This leaves seniors financially and susceptible to pitfalls such as over or under spending and overlooking the material impact of inflation.

A recent study by the Canadian Public Pension Leadership Council on Canadians’ perceptions on retirement found that many are uncomfortable relying on family for financial support or using social programs that are already over-taxed. Yet the uncertainty and unpreparedness for inflation and new expense pressures can drastically erode purchasing power over time and create stress on social programs.

Why is it important to act now? Many boomers have recently entered their retirement era and more Canadians will be joining them soon. With more than one in five working adults now nearing retirement and people living longer than ever before the need for comprehensive, longevity-oriented retirement literacy and solutions is urgent.

Industry innovators can aid and educate Canadians in an impactful way by designing solutions that meet the real needs of seniors and mitigate pitfalls, supporting both the supply and demand side of the retirement income security. Reducing barriers to efficient investments in retirement so that Canadians can convert savings to lifetime retirement income and earn a return as they age is a leap towards a more sustainable future.

Sources:

Retirement Survey, Scotiabank, February 2020

The Social Implications of Pensions, Robert Brown, February 2019

Affordable Lifetime Pension Income for a Better Tomorrow: How We Can Address the $1.5-trillion Decumulation Disconnect in the Canadian Retirement Income System with Dynamic Pension Pools, National Institute on Ageing, November 2021

The Pensions Canadians Want: Perceptions on Retirement, Canadian Public Pension Leadership Council, June 2023